Are you ready for SAP S4 HANA in the Cloud - SUBNAV

63%

of organizations are targeting cloud variants of SAP S/4HANA

91%

of organizations want independent strategic oversight for their S/4HANA transformation

55%

of organizations position AI as core to their S/4HANA vision

The industry distribution of participating companies certainly influences migration patterns. For instance, regulated industries often show distinct preferences in deployment models—particularly around data residency, compliance requirements, and risk tolerance for public cloud adoption.

When it comes to migration, organizations span the full implementation life cycle (see figure 2). The largest segment (28 percent) is in the implementation phase, followed by those in contract negotiations with SAP (21 percent) and active planning (19.5 percent). Eighteen percent report being live on S/4HANA, while 11.5 percent are in the process of selecting vendors. Only 2 percent have not yet started their journey.

Organizations are pursuing three primary migration approaches: greenfield implementations, or starting fresh with new systems; brownfield conversions, which involve upgrading existing systems in place; and bluefield conversions, which uses selective data transformation.

Greenfield accounts for 37.5 percent of planned migrations, brownfield represents 29 percent, and bluefield makes up 23.5 percent (see figure 3). The remaining 10 percent have not yet determined their migration strategy—which should be a major concern for these enterprises with the 2027 deadline fast approaching.

Our survey results clearly reveal an emerging new trend. The combination of brownfield and bluefield approaches is the dominant path to the future state. The reason? Companies are seeking faster, lower-cost options to upgrade as they face more economic pressure and uncertainty, combined with the looming support deadline.

On the other hand, the greenfield approach is especially favored by companies currently on SAP ECC with a highly fragmented technology ecosystem. Data quality and legacy complexity issues, cited as two of the top three business challenges by SAP ECC companies, are likely strong motivators for this group to pursue a clean reset via greenfield.

Figure 3: Intended migration path

And where are companies headed? When examining their intended target states, we see a clear preference for cloud-based deployments, with an aggregated 63 percent of organizations targeting cloud variants versus 37 percent planning to remain on-premise (see figure 4). SAP S/4HANA RISE (private cloud) is the leading choice, with 46 percent of organizations planning this deployment model, followed by on-premise S/4HANA at 37 percent and SAP S/4HANA GROW (public cloud) at 17 percent.

Indeed, the lure of the cloud is strong. We found that even companies that are already using on-premise S/4HANA are overwhelmingly open to RISE or GROW as a target end state and to consider greenfield migrations to RISE.

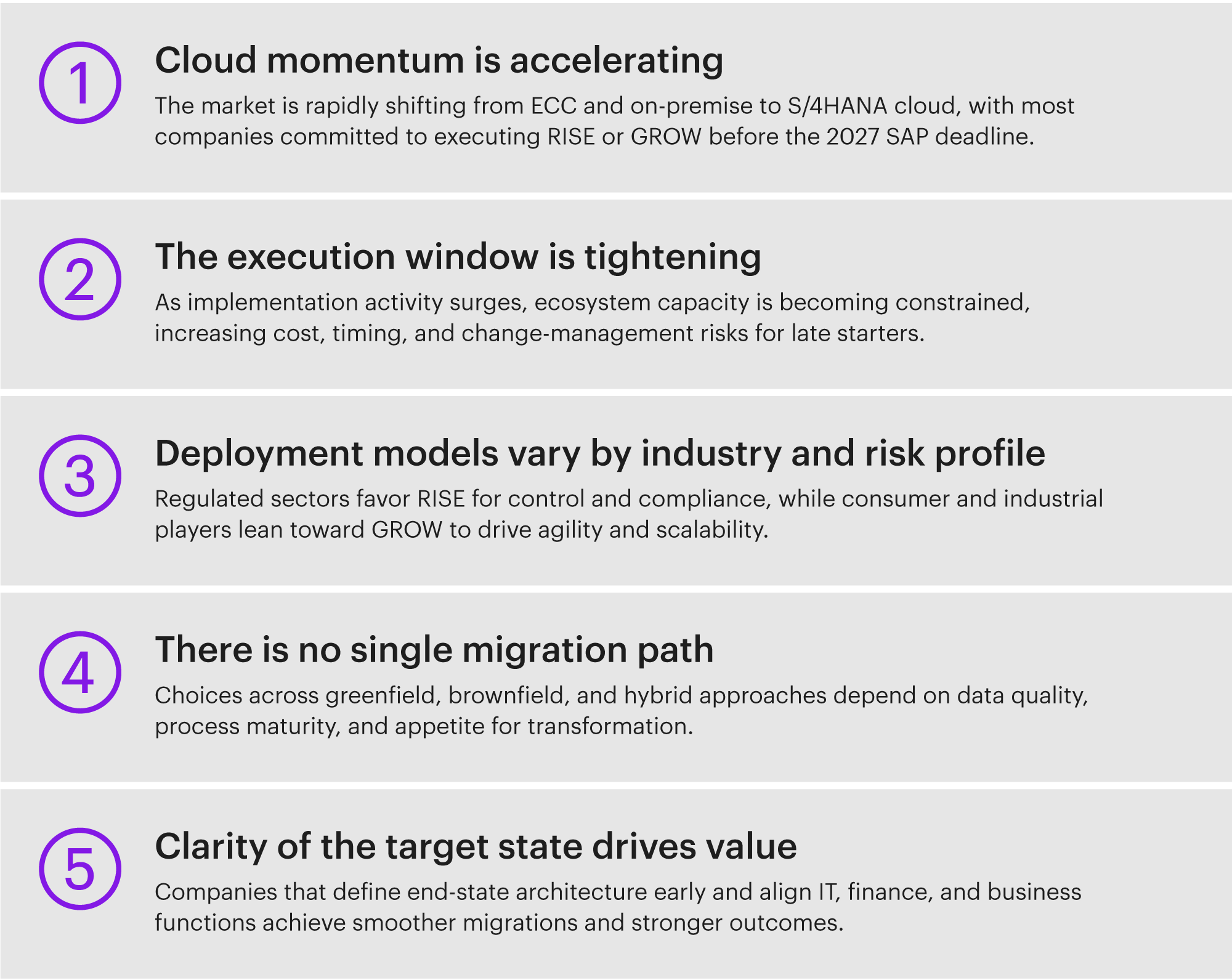

Key takeaways: