Global Trends 2020-2025 - Body Part 1

Executive summary

- Embattled governments. Crises of rising inequality, climate change, and now COVID-19 are converging to place unprecedented levels of fiscal and political pressure on governments throughout the world. As fiscal deficits persist through 2025, national governments increasingly constrained by stock of debt and fewer economic policy prerogatives will turn to local administrations and the private sector for support to maintain public trust.

- Push to national self-sufficiency. The pandemic has served as a wake-up call to national governments on the need for self-sufficiency and resilience in the face of crisis. As governments move to improve their domestic capabilities in key sectors—healthcare, technology, food, energy, and manufacturing—the private sector may find opportunities for increased collaboration with government. Too much government intervention, however, could stifle innovation in the long run.

- Stranded segments of society. Over the next five years, growing inequality—exacerbated by COVID-19—will lead to further marginalization of stranded segments of society, including minorities, low-skilled workers, students, children, working mothers, and others. Reintegrating them will be a tall order in a weak economic environment, but it behooves governments and businesses to work together to re-skill and reposition these important groups in society.

- Rise in food insecurity. A global food crisis is on the horizon, with disproportionate downside implications for emerging markets. Food supplies are tightening due to trade restrictions and COVID-induced production disruptions, and incomes are falling amid economic turmoil. The five-year outlook suggests the situation will get worse, resulting in changes in the food industry, widening inequality between countries, and depressed productivity overall.

- Industry consolidations, mergers, and acquisitions. The economic disruption brought about by the pandemic has weakened finances for businesses across the world. This trend will result in a wave of industry disruption and consolidation as stronger companies acquire weakened rivals, technologies, or assets—with private equity, big tech, and the energy industry poised for the biggest shakeouts over the next five years.

Trend #1

Embattled governments

COVID-19, global protests of systemic inequality, climate change, and widespread economic woes ranging from income stratification to unemployment. These are just a few of the issues placing staggering burdens on federal, regional, and city governments throughout the world. While some are crumbling under the pressure, others are making use of policy and technology to ensure they get through the pandemic while mitigating human and economic loss. Over the next five years, governments will have to contend with massive macroeconomic and health constraints while maintaining or rebuilding the trust of their citizens as the fallout from COVID-19 and social injustice protests persist. This test will be central in the coming great shakeout over the course of pandemic recovery, with implications not only for which countries emerge stronger or weaker but also for the global operating environment overall.

Government policy in an uncertain world

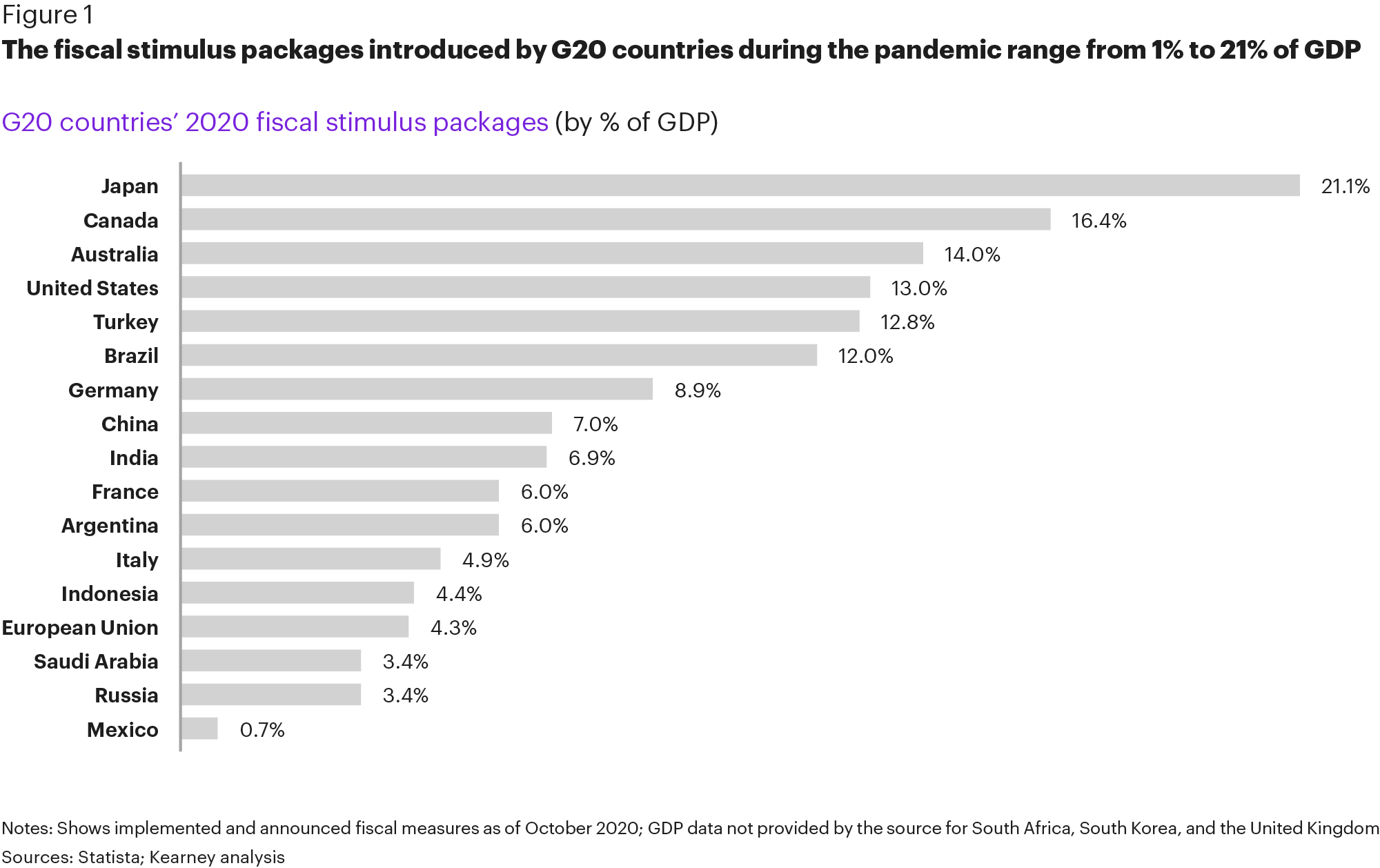

As the COVID-19 pandemic assails governments throughout the world, many leaders are employing fiscal and monetary tools to temper the economic fallout (see figure 1). The scale of the fiscal interventions is impressive—and is perhaps marking a reemergence in popular support for “bigger” government. Japan, for example, has introduced a fiscal stimulus package amounting to more than 20 percent of its GDP. The United States has funneled an estimated $2.3 trillion into the Coronavirus Aid, Relief and Economy Security (CARES) Act, though momentum on a second tranche is uncertain at the time of this writing. And the European Union (EU) announced a €750 billion Next Generation EU recovery fund.

The scale of monetary policy interventions is no less impressive. At the end of March 2020, the United Kingdom cut interest rates to their lowest level ever—0.1 percent—to keep borrowing costs down for government and business. Many other countries have followed suit, with some such as Chile and Peru on the verge of negative real interest rates as a result of monetary easing and inflation dynamics. In the United States, the Federal Reserve has announced a major policy shift to average inflation targeting, which means that it may allow inflation rates to exceed 2 percent before raising interest rates.

Governments are also calling on the private sector for support. Many Western governments are taking policy actions that are unprecedented outside of wartime, such as repurposing production to essential goods and seizing supply chains to produce or procure emergency equipment. The United States, for example, has relied on the Cold War-era Defense Production Act to shift production to medical equipment, mandating General Motors to construct ventilators and 3M to fabricate N95 respirator masks for the federal government—efforts that could be expanded in the future. The German health system has relied on private-sector laboratories to analyze far more COVID-19 samples than any other country. And at the beginning of the crisis, Nigerian private sector companies joined together to create the Coalition Against Coronavirus (CACOVID) in order to complement government efforts to spread awareness about the virus and support healthcare institutions.

Governments’ expanded fiscal and monetary policy actions amid COVID-19 are likely to continue over the next five years, which could lead to further challenges down the road. Advanced economies may be able to sustain additional debt burdens and low interest rates for some time, but these bills will eventually become due. While these measures are necessary to navigate this present moment of crisis, they will grow more difficult to sustain for a long period as debt mounts. Emerging markets face more immediate challenges as funds run dry sooner and borrowing opportunities are more limited. Additionally, their currencies are less accepted globally, leaving them with less room to maneuver than their more developed counterparts.

Implications of overstretched governments

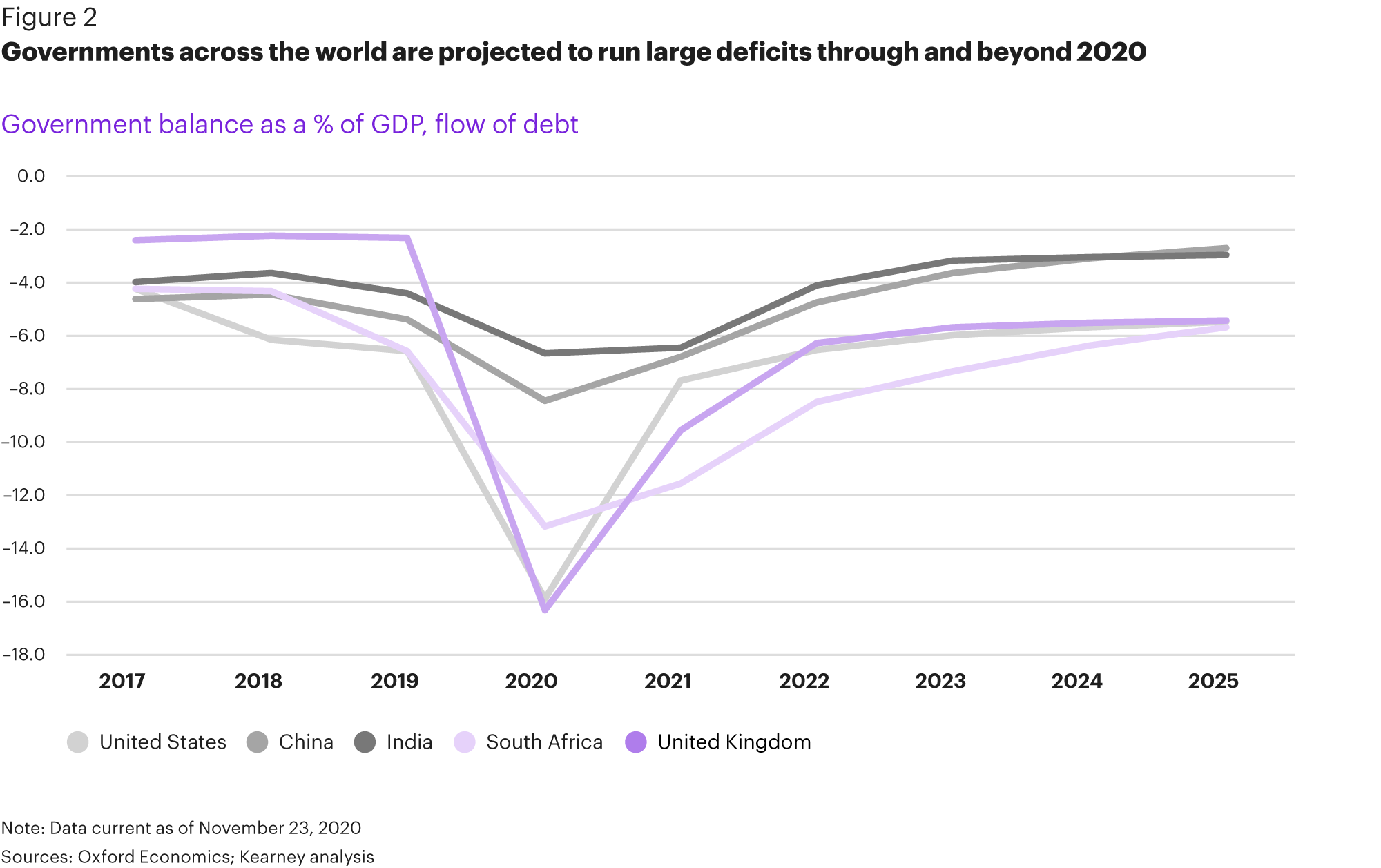

Between 2019 and 2020, government deficit levels have grown dramatically as a result of the extreme fiscal and monetary measures taken to combat the economic impact of COVID-19 (see figure 2). The implications of these rising government deficits could be significant both in macroeconomic terms and to key sectors affected by public finance. In the United States, the federal deficit has reached 17.9 percent of GDP in the 2020 fiscal year—a figure almost twice as large as the highest seen during the Great Recession (9.8 percent) in 2009. As of October, the United Kingdom was facing its highest debt-to-GDP ratio in 50 years. And South Africa’s growing debt burden—which could reach 84 percent of GDP by the end of fiscal year 2020—is reducing the government’s ability to offer further support to its state-owned enterprises such as power utility Eskom and South African Airways.

Such soaring deficits are expected to continue through 2025 for many advanced economies. The implications of this budget overstretch are jarring. It could lead to a loss of trust in government overall, a tendency that has historical precedent. As a result of the 2008 financial crisis, for example, levels of mistrust toward the European Commission (EC) rose from 27 to 47 percent between 2007 and 2013. And it may be worse this time around. According to a Kantar survey, people across almost all of the world’s leading advanced economies have become more skeptical about their governments’ handling of the coronavirus pandemic over time. In the Group of Seven (G7) nations in May, only 48 percent of respondents approved of authorities’ handling of the pandemic, down from 54 percent in March.1

As federal governments become more financially constrained and public trust deteriorates, they may rely on local administrations to share the burden of leading through the crisis. While a recent Edelman survey found increasing aggregate trust in governments overall, in places where trust in the federal government was lacking, local government filled the void. This held in countries including the United States, Japan, and France. Indeed, cities across the world are taking on an outsized role during the pandemic as they carry out contact tracing, institute lockdowns, and care for the vulnerable in their respective populations. To keep local governments operating effectively, federal governments may increasingly need to provide funding support. Estimates from the World Bank and UN entities suggest that local governments may on average lose 15 to 25 percent of revenues in 2021 owing to COVID-induced economic turmoil.

There is reason for optimism, however. Despite concerns about inadequate funding or even insolvency, city governments around the world have been stepping up throughout the COVID-19 crisis, increasing pedestrian access, building makeshift hospitals, and providing housing for the homeless. Houston, Texas, for example, has developed a new initiative known as the COVID-19 Community Health Education Fellows (CHEF), designed to educate and empower at least 100 youth and young adults to help the city fight COVID-19, particularly in the most vulnerable communities. The private sector is also involved in this endeavor, as JPMorgan Chase has provided a $100k grant to the program. Such measures are not restricted to cities in advanced economies. Despite limited funding, Kigali placed numerous portable sinks for handwashing at bus stops, restaurants, banks, and shops across the city. And in Monrovia, the Cities Alliance has relied on social mobilizers to spread the word in informal settlements about basic hygiene practices. As pandemic recovery progresses, federal, provincial, and city governments globally—in concert with the private sector—will need to find ways to strengthen their cooperation to meet both the immediate and longer-range challenges posed by the pandemic.

The outlook

As governments take on additional responsibilities through and beyond COVID-19, they’ll face mounting economic, political, and social challenges. Further, embattled governments will need to find new ways to work together and engage in multilateralism to rebuild international institutions in a way that is sustainable and appropriate for the 21st century. They need to retool domestic capacity to make it more resilient as well (see Trend #2). Even with renewed efforts on the part of multilaterals, maintaining public trust in government will be a persistent challenge. To mitigate this stress, governments increasingly will rely on the private sector to re-skill the unemployed, especially stranded segments such as low-skilled workers (see Trend #3). Such cross-sector collaboration will also be necessary to develop and deploy contact-tracing technology, PPE, and vaccines. There is reason to hold out hope that the great shakeout could result in renewed multilateralism and increased government efficiency. Such efforts will be required if embattled governments are to survive the challenge ahead.

Business implications

- Businesses will take on functions that governments cannot. As governments become more financially constrained over the next five years and beyond, businesses will assume additional responsibilities to support and fill gaps—even in the absence of government regulations to guide their activities. Indeed, businesses are already supporting governments in initiatives to combat COVID-19. In May, Google and Apple announced a joint effort to enable the use of Bluetooth technology to help governments and health agencies reduce the spread of the virus. Technological and cash support to vulnerable segments will continue as businesses recognize the reputation and financial gains that follow.

- Companies will harness stimulus funds to rebuild. As beleaguered governments inject cash into diverse sectors ranging from travel and tourism in the United States and Europe to renewable energy in South Korea, businesses will take advantage of upcoming fiscal stimulus bills and identify strategies to best apply for and benefit from this government support. “Green” recovery programs will also involve the private sector, as governments offer financial support to businesses for energy efficiency improvements and installation of renewable energy systems. Such advances in the circular economy in turn help governments meet climate and sustainability goals.

- Small and medium-sized businesses (SMBs) will seek out creative funding sources to fill in government funding gaps. Though many governments throughout the world have provided emergency funds to a variety of SMBs, the support often has not been enough. Therefore SMBs will increasingly look for financing from other sources, such as through GoFundMe’s Small Business COVID Relief Initiative, microloans, and venture capital funding. As governments become even more embattled over the next five years, innovative SMB funding methods and sources will only grow in number and popularity.

Trend #2

Push to national self-sufficiency

Governments around the world face encumbered supply chains, scarce medical supplies, and a race to health and recovery. The COVID-19 pandemic has served as a wake-up call to national governments on the need for self-sufficiency and resilience in priority economic areas, including medical goods and technology. This push toward producing more goods at home, using domestic companies, will only increase in the next five years over the course of the great shakeout brought about by the pandemic. New policies to boost domestic capabilities in key sectors such as healthcare, technology, agriculture, energy, and manufacturing could have a positive impact on the economy by supporting emerging industries and minimizing the risks of globalized supply chains. Yet there are also risks of too much government intervention, which could disincentivize innovation and artificially prop up inefficient “national champions.” It’s as yet unclear where governments will fall on this spectrum, but there’s little doubt that these shifts toward greater self-sufficiency are underway.

The pendulum swings away from the world and back toward the state

From the late 1980s to the Great Recession of 2008, globalization defined the business-operating environment. As the world grew more connected following the fall of the Soviet Union, the creation of the North American Free Trade Agreement, and China’s entry to the World Trade Organization, statist policies were abandoned in exchange for free trade and global value chains. After the financial crisis, however, the pendulum began swinging away from globalization. As former US Secretary of State Henry Kissinger wrote in 2008, “globalization tempts a nationalism that threatens its fulfillment.” In the years that followed, populist leaders worldwide rose to power advocating against globalization, immigration, and open markets. The US–China trade war, Brexit, and the rise of industrial policy worldwide are just some signals of this shift. Rather than relying on international connectedness, countries started to look for opportunities to re-shore in order to bolster domestic capabilities, and they began preparing for further trade protectionism. Then COVID-19 arrived.

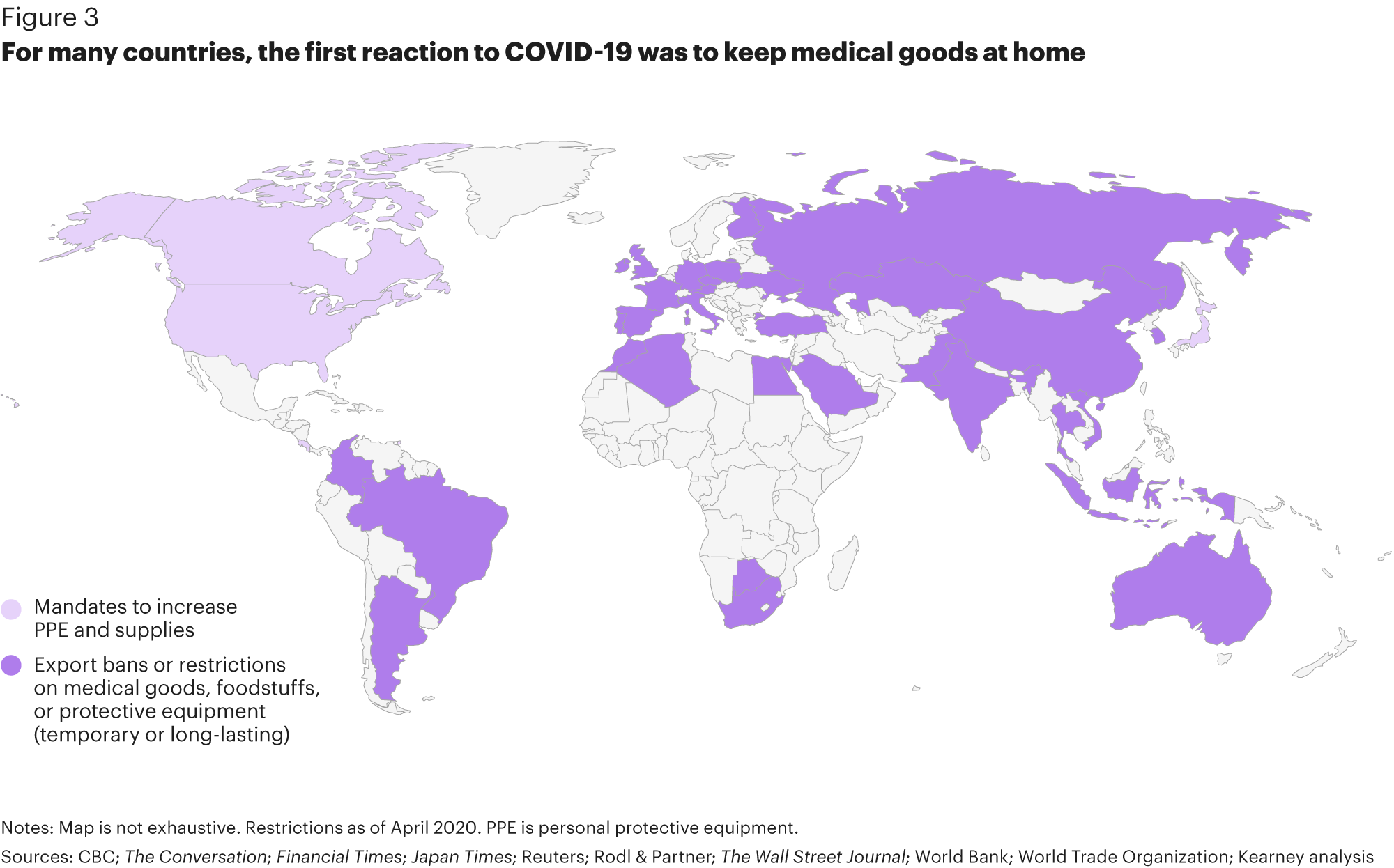

The virus has since spurred rapid shifts toward domestic capacity in key sectors, most notably in healthcare and technology. Springtime shortages of medical equipment have prompted governments to beef up national supply chains and stockpile materials (see figure 3). Some are investing in vaccine research, including Russia, China, and India (which is funding vaccine trials for local companies like Bharat Biotech). India’s Serum Institute, moreover, is working to mass-produce a coronavirus vaccine, half of which will be reserved for Indians, with the other half for emerging markets. The United States has mandated that US companies such as General Motors use their plants to produce ventilators under the US Defense Production Act to ensure sufficient domestic capacity without relying on imports, though critics have argued that this mandate was insufficient to meet demand. And in the EU, Brussels has advised member states to be wary of foreign direct investment in medical fields out of fears that foreign ownership could direct these products abroad. In light of the much-celebrated news from Pfizer and Moderna in November showing that their vaccines appear to be highly effective, a number of countries either have existing agreements or are reaching deals with these companies to provide the vaccine to their populations. This includes the United States, Canada, Japan, and the United Kingdom, along with the European Union, though their respective health authorities must approve the vaccine before it can be administered. If further developments are announced, more national supply deals are likely.

Apart from medical goods, the pandemic has also underscored the need for modernized domestic technology infrastructure. From contact tracing and health data analysis to communications facilitation during shutdowns, technology has been crucial to navigating the pandemic. National efforts to support domestic technology and restrict foreign products were already underway pre-COVID, exemplified by the international competition to develop 5G, US sanctions on Huawei, and the EU’s plans for “technological sovereignty” to develop digital capabilities that could match those of China and the United States. The pandemic has simply accelerated these trends. In June, US legislators proposed more than $22 billion in tax breaks and grants to support domestic chip manufacturing in an effort to build national self-sufficiency, citing vulnerabilities in existing supply chains and reliance on trading partners like China. China, on the other hand, has leaned on domestic tech companies for contact tracing efforts. And in Europe, the EU provided €164 million in R&D funding to coronavirus-focused tech start-ups based in EU member states and associated countries. Governments increasingly see domestic technology capacity not just as important for their population’s well-being but also as a crucial component to compete in the world economy and protect national security.

Countries will seek self-sufficiency in more fields to contend with future crises

Beyond the immediate need for increased medical and technological self-sufficiency, countries are looking at boosting other industries that will mitigate future crises—food, energy, and manufacturing chief among them. Some are taking measures to strengthen domestic food production, particularly as food insecurity worsens (see Trend #4). Though agricultural subsidies for domestic farming were well established before the pandemic, countries are now expanding such programs. For instance, the EU has raised agricultural aid to maintain domestic production, giving the hardest-hit farmers up to €7,000. Some member states have gone even further: lawmakers in the Czech Republic have introduced a bill that would require at least 85 percent of food on retailers’ shelves to be produced domestically by 2027. Across the Atlantic, the United States has launched the Coronavirus Food Assistance Program to disperse up to $16 billion in direct relief to domestic farmers and ranchers. Importers in the Middle East have also considered boosting local food production through tariffs and improving farming infrastructure, and Singapore is investing more in vertical farming to improve food security. National investment in domestic food production is only likely to grow in the coming years as food insecurity worsens worldwide, and especially if trade protectionism remains.

National self-sufficiency efforts in the energy sector, also long-standing, have become a part of pandemic economic recovery efforts in several countries. The United States, for example, pursued a policy of energy independence before COVID-19 with the goal of reducing reliance on energy imports. Early in the crisis, oil prices dropped to historic lows due to plummeting demand driven by stay-at-home orders. To support its domestic oil industry, the United States took the historic step of involving itself in OPEC+ discussions to lift prices.2 Europe, on the other hand, is looking to boost its renewables sector by incorporating parts of its European Green Deal into its COVID-19 recovery plans. The bloc intends to fund green projects such as the North Sea Wind Power Hub Programme, an initiative led by EU companies that will receive €14 million to increase offshore wind production. This effort will not only advance the region’s climate goals but also help diversify energy sources by supporting European companies, a win-win for greater energy self-sufficiency. South Korea has taken similar steps to help domestic companies compete in green technologies. The country’s Green New Deal, for example, aims to have at least 1.13 million electric vehicles on the road by 2025, which will likely help national firms such as Hyundai and Kia as they expand their electric fleets.

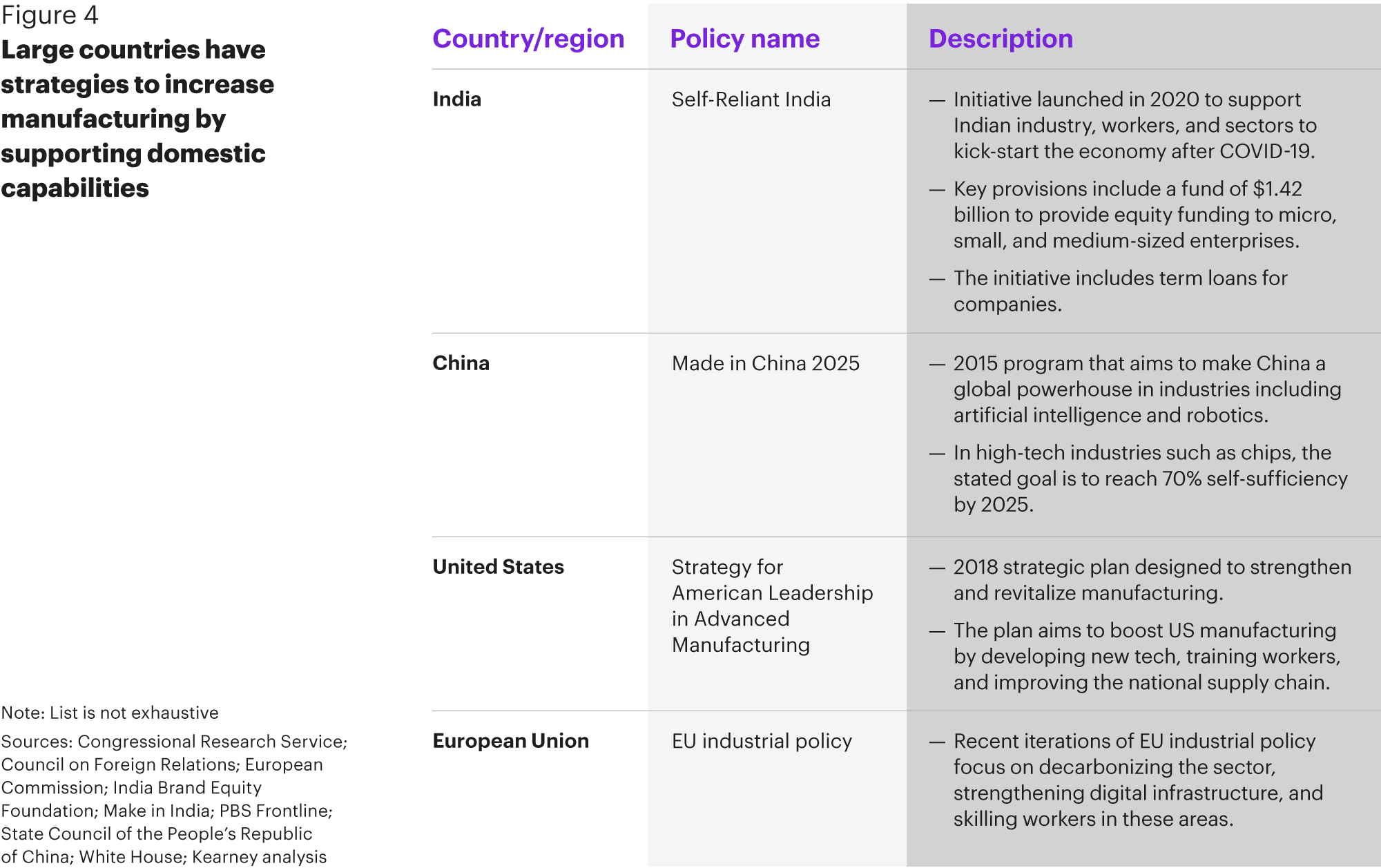

Countries also see manufacturing self-sufficiency as necessary to surviving future shocks (see figure 4). Shortly after COVID-19 struck, Japan started subsidizing companies to move production out of China in the hopes of stabilizing supply shocks. One company alone, Sharp Corporation, is slated to receive more than $536 million in this effort. India has also updated policies to increase domestic electronics production, which is aligned with its 2014 Make in India initiative. In May, the country unveiled a plan to support domestic industry through the Self-Reliant India program, which supports small and medium- sized enterprises through subsidies and tax breaks. In the medium term, these efforts will only grow as geopolitical tensions remain fraught and countries search for ways to kick-start economic growth post-pandemic.

The outlook

As the pendulum swings further toward a state-centered economy, we can expect to see more government investment in the five industries mentioned—namely healthcare, technology, agriculture, energy, and manufacturing (and potentially a few others, including infrastructure). This investment will likely add to the pressures already faced by embattled governments around the world (see Trend #1). Long, multinational supply chains are highly exposed to global risks such as an international pandemic, and external shocks show no signs of abating in the next five years. Government support for domestic industry is an attractive risk-mitigation measure and could help indigenous industry take off, creating more jobs and development. Yet it can also be costly and, if the pendulum swings too far, could create other challenges. Too much government intervention could keep inefficient and unproductive industries afloat by eliminating competition and disincentivizing innovation. And eventually rolling back such subsidies could prove politically challenging. In the next five years, the great shakeout will result in increased government intervention and moves toward self-sufficiency. It will be incumbent on strategic businesses to monitor just how far this pendulum swings.

Business implications

- Companies will face greater pressure to localize supply chains. National governments may continue to offer incentives to companies that choose to localize production. These incentives are already taking place in Japan, the United States, and parts of Europe, as governments look to rebuild manufacturing capacity and minimize disruptions from multinational value chains. Re-shoring or near-shoring will likely continue as barriers to trade and increased geopolitical tensions remain. This trend will create opportunities for companies that can relocate closer to home, and provide additional benefits such as the ability to better monitor environmental and labor standards.

- Businesses may have trouble using and sourcing foreign tech, especially components such as chips. As technological competition intensifies, strategic companies will consider where they source their component parts such as semiconductors. Efforts like those underway in the United States to boost domestic chip production will continue, while export controls could become more common in much of the world, including in China. If countries take more steps to restrict foreign technology’s access to domestic markets, companies may be encouraged to buy locally made goods over imports.

- Manufacturing could make a comeback in advanced economies. Though many advanced economies are service based, further government support in manufacturing and emerging Fourth Industrial Revolution (4IR) technologies such as digital twins could help the sector revive. This is particularly true in areas such as chip manufacturing, electronics, minerals processing, and the automotive industry, as these companies look slated to receive significant government support in the next five years. Companies can take advantage of this support by investing in manufacturing opportunities in advanced economies, as some firms such as TSMC are doing.

Trend #3

Stranded segments of society

Far from being a great equalizer, COVID-19 has disproportionately affected the world’s most vulnerable. As global poverty levels rise to new heights, inequality is growing, fueling protests and riots from the United States to Australia. Over the next five years, this inequality will worsen, exacerbated by COVID-19, and lead to further marginalization of already stranded segments of society in both advanced and developing economies—including ethnic minorities and low-skilled workers. In parallel, new segments such as students, children, and working mothers will also find themselves stranded as the virus restricts opportunities for learning and earning. As these groups fall victim to the great shakeout, there will be increased pressure for governments and businesses to work both independently and in concert to support them.

Multiple segments of society are becoming stranded

Minorities, and more specifically Black and Latinx people, have long experienced economic and social inequity in many countries; the virus is exacerbating these inequalities. In the United States, for example, a Pew Research study conducted in April found that 73 percent of Black Americans did not have emergency funds to cover three months of expenses during the pandemic, while only 47 percent of white adults said the same. Disparities are also evident in contraction of the virus—Black Americans represent roughly 14 percent of the population but around 30 percent of COVID-19 cases. And the National Bureau of Economic Research found in the same month that US Latinxs were disproportionately affected by the COVID-19 recession, experiencing an unemployment rate of 18.2 percent compared to the national average of 14.2 percent. These challenges are not limited to developed markets. In South Africa, predominantly Black townships were much harder hit by the pandemic than primarily white areas, and in Brazil COVID-19 deaths were disproportionately high among Black and mixed-race patients. Along with COVID-19, structural racism is inciting protests throughout the world as these stranded segments fight not only a disease of the body but also systemic problems that require massive policy interventions to address.

Low-skilled workers in both advanced and emerging markets, many of whom were already weathering the left-right punches of outsourcing and automation, are also facing disproportionate COVID-era challenges. Even before the onset of the pandemic, Oxford Economics predicted that 20 million global manufacturing jobs could be lost to robots by 2030. And low-skilled workers may be stranded from their jobs at even higher rates as automation ramps up. Call centers, from Manila to Bangalore and beyond, are on the decline during the COVID-19 crisis as chatbots take over. Moreover, restaurants, hotels, and food services are among the establishments around the world that employ large numbers of low-skilled workers who are now faced with unemployment. According to the US Department of Labor, by September, workers with bachelor’s degrees or higher had nearly fully recovered jobs lost in early spring. However, those with just a high school diploma held 11.7 percent fewer jobs in September than in February. As contactless technology becomes more popular, workers such as delivery drivers and supermarket employees could see similar job displacement. Dutch grocer Ahold, for example, is accelerating development of a robotic order processing arm that can scan and stock shelves.

As these technological developments cause massive job displacement among low-skilled workers, the private and public sectors will feel pressure to find ways to reintegrate these workers and other stranded segments into the economy.

Students, recent graduates, and children are among the new groups to face growing marginalization. A global survey released by Save the Children in September indicated that more than 1.6 billion learners have faced school closures due to the pandemic, with fewer than 1 percent of children from poor households having access to the Internet for distance learning. University students and recent graduates are also facing challenging futures. Indeed, it is likely that Gen Z will de-prioritize college and university education (at least in the early post-COVID world) as in-person classes are limited. In the United States, a higher education trade group has predicted a 15 percent drop in university enrollment nationwide, including many foreign students unable to return for their studies, which will amount to a $23 billion revenue loss for colleges. Recent graduates are also hard hit, with two-thirds in the United Kingdom seeing a job application withheld or put on hold as a result of the virus.

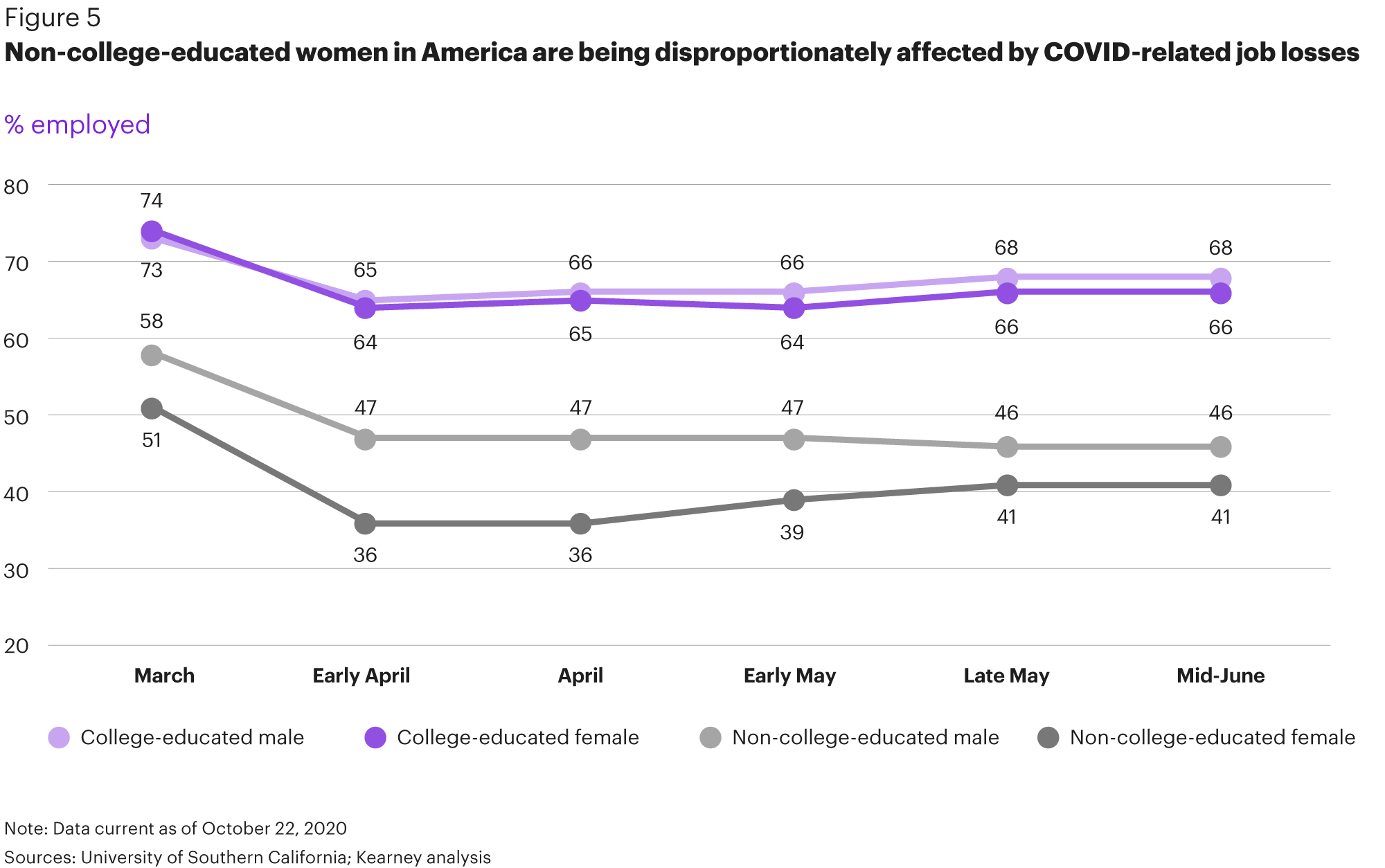

Additionally, children’s learning from home has upended the lives of many working parents, especially mothers, in both advanced and emerging economies. Among married couples who work full time, women provide close to 70 percent of childcare during standard working hours—a burden that has grown considerably as schools and other activities have shut down amid COVID-19. Indeed, in September, more than 860,000 women dropped out of the workforce in the United States, citing the need to care for children at home. Non-college-educated women have been hit especially hard by job losses in the United States (see figure 5). And in the developing world, the departure of many women from jobs in the informal sector is leading their families into financial ruin, with gender poverty gaps expected to widen even further by 2030.

A multisector response to reintegrate the stranded

Stranded segments will continue to decouple from the global economy over the next five years unless the government, international institutions, and the private sector all work both independently and together to reintegrate them. This effort includes taking action to support integration of racial and other minorities. Some modest steps have already been taken. For example, in response to the summer protests throughout the world combating structural racism, politicians have ordered the removal of Confederate statues in the United States and promised police reform. Japanese fashion retailer Uniqlo joined forces with the ACLU and committed to donating $100,000 to organizations that aid the Black Lives Matter movement. Adidas has said it will fill at least 30 percent of its open positions with Black and Latinx employees. And Apple and Japanese giant SoftBank have both pledged $100 million to minority-owned businesses and those promoting diversity. These moves will not solve long-standing and deep-rooted problems of racial inequity in and of themselves, but they do represent steps in the right direction.

For low-skilled workers, forward-thinking governments and businesses are focusing on re-skilling initiatives to ensure that stranded employees are able to progress in a more automated post-COVID world. Sweden has taken an early lead in forging a public-private re-skilling alliance during the pandemic. The partnership between HR and search firm Novare Human Capital and Sophiahemmet University offers a basic medical training program for SAS (Scandinavian Airlines) cabin staff to transition into assistant nurse roles. And Microsoft has pledged to offer digital skills training for 25 million people worldwide by identifying the most in-demand skills ahead of the COVID-19 unemployment surge and offering relevant courses accordingly.

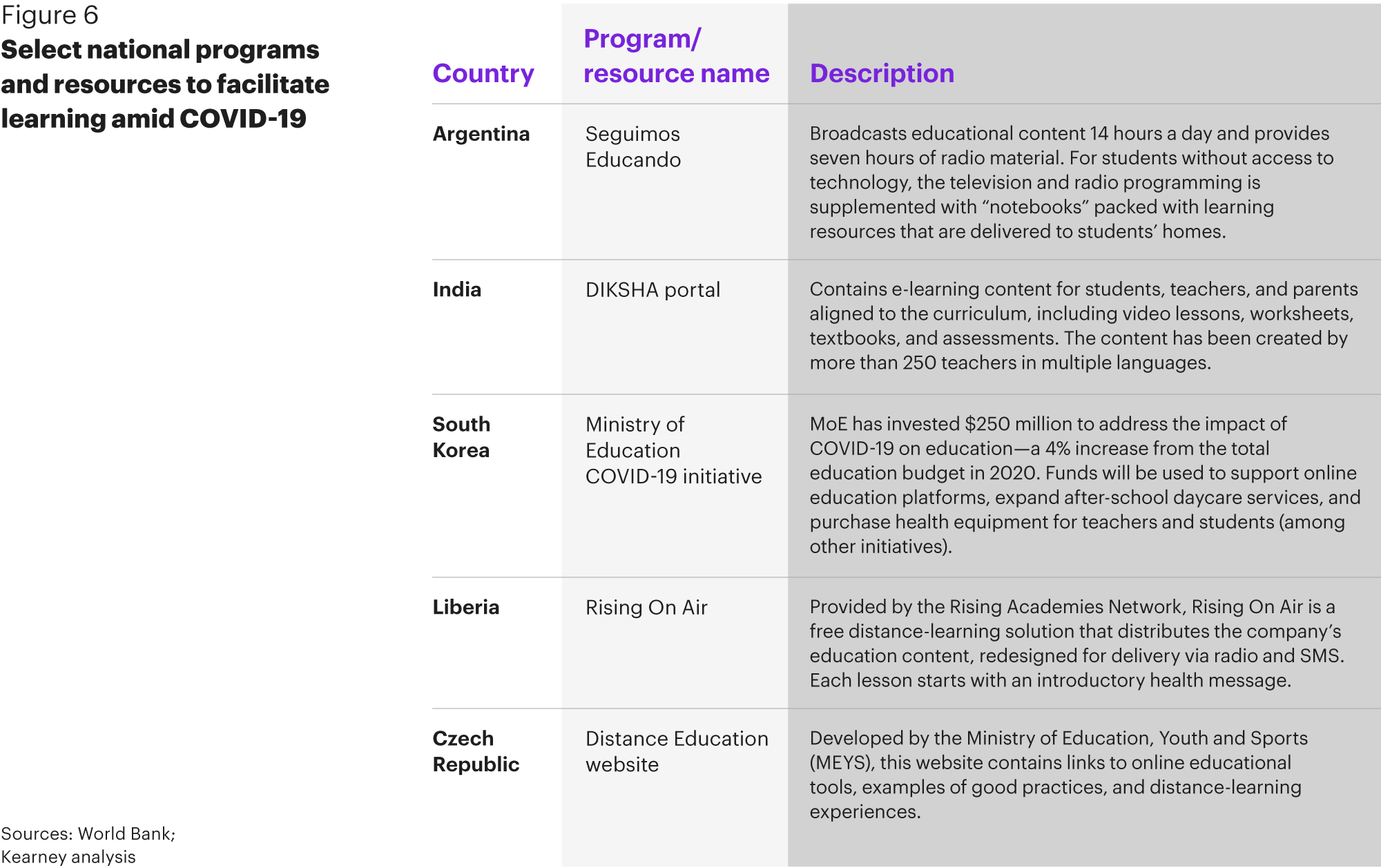

Students and children will also need the support of both public and private institutions to avoid being further stranded. To that end, UNICEF and Microsoft have conducted an early launch of their Learning Passport program, which helps facilitate online learning in countries where the curriculum can be digitized. Timor-Leste, Ukraine, and Kosovo were the first to release their online curricula through the program. And national governments are creating their own resources to help online and on-site learners (see figure 6). Argentina, for example, has introduced Seguimos Educando, which bridges digital gaps by offering notebooks filled with learning materials to students without adequate access to technology. Initiatives such as these will ensure that educational and digital inequality do not negatively affect students’ prospects when they eventually enter the workforce.

Finally, governments and businesses can ensure that working mothers do not become further stranded by subsidizing childcare to keep them in the workforce. Important benefits beyond subsidies or onsite childcare could include flexible work schedules, more predictable hours and schedules, backup childcare assistance, and flexible childcare spending accounts. Google, for example, has already made strides in this area, having expanded its paid family caregiver leave policy by eight weeks. Governments, in both advanced and emerging economies, can help working mothers by boosting funding for primary schools so they can open safely and providing federal funding to childcare providers (among other initiatives).

The outlook

As COVID-19 persists, several countries and businesses are using recovery mechanisms to address the institutionalized inequality that has existed throughout the world for far longer than the virus. Much work remains to be done. Social movements such as Black Lives Matter, public-private partnerships, and economic recovery measures from COVID-19 may prove beneficial, but centuries of deeply entrenched inequality will take far longer to address on a meaningful scale. Some stranded segments may never be fully reintegrated into society. For example, large numbers of low-skilled workers may not have the means or opportunities to re-skill. If many of these groups continue to be alienated or stranded, we could see more of a drift toward populism or nationalism—in emerging and developed markets alike—as they feel victimized in a post-COVID environment. While there are still opportunities to avoid these worst outcomes following the great shakeout, strategic businesses and governments would do well to prepare for these scenarios—and at the same time work alongside other stakeholders to prevent them.

Business implications

- Leadership will be held to new standards. Strong public and private sector leadership is vital to reintegrate stranded segments, and consumers will increasingly call for just that. Indeed a recent global study found that consumers are four to six times more likely to buy from and defend “purpose-driven businesses” dedicated to something more meaningful than products and services. In order to address the need for more inclusive representation and societal demands for greater tolerance, business leaders will therefore vocalize the need for nondiscriminatory behavior in the workplace and push for greater diversity on boards.

- Companies will focus more on their childcare benefits and offerings. Over the next five years, companies will increasingly take tangible steps to improve their childcare support and offerings for working parents—in no small part to disincentivize mothers from leaving the workforce due to heavier burdens at home. Hubspot, for example, is already taking innovative steps in this direction by offering virtual events for children such as story times or sessions in which they learn about outer space. These virtual events give parents more time to focus on work.

- Re-skilling and workforce training will be prioritized. Given the devastating impact of COVID-19 on minorities, students and recent graduates, low-skilled labor, and other groups, companies will work independently and with governments to promote re-skilling, joining initiatives such as the World Economic Forum’s Re-skilling Revolution. This multi-stakeholder effort aims to provide one billion people with education, skills, and jobs over the next decade by connecting and coordinating re-skilling initiatives at scale. The urgency for such programs and others like it will grow as automation eliminates jobs and displaces laborers.

Trend #4

Rise in food insecurity

Disrupted supply chains, lockdowns, rising prices, and shortages are just some of the ways that COVID-19 is exacerbating food insecurity. As the great shakeout upends governments and business, food insecurity is rising, widening economic disparities and weakening productivity. The World Food Programme, the 2020 Nobel Peace Prize winner, estimates that 265 million people could face food insecurity this year, up from 130 million in 2019. Export restrictions and stockpiling have the potential to tighten food supply as more people struggle to pay for goods given the economic downturn. And while food insecurity has global implications, emerging markets are particularly vulnerable given their existing rates of hunger, dependence on remittances, and large agricultural sectors—all of which are facing additional pandemic-driven stresses. These dynamics have direct business implications—from decreased productivity to a rise in absenteeism in the workplace. And the food industry itself is also changing to accommodate limited consumer spending power amid the pandemic, from offering discounts to changing package sizing and reducing food waste.

Even after the virus recedes, food insecurity is here to stay

Before COVID-19, consistent progress had been made in reducing global hunger, food insecurity, and malnutrition, despite some setbacks in recent years. The proportion of undernourished people worldwide had been declining rapidly until 2015, when it reached 11 percent. Since then, the absolute number of those experiencing hunger has increased to 820 million in 2018, from 795 million just three years earlier.3 The challenge is particularly pronounced in emerging markets owing to high rates of poverty and conflict. In sub-Saharan Africa, almost 23 percent of the population is hungry, and in Southern Asia, the proportion is 15 percent, representing roughly 239 and 279 million people, respectively.

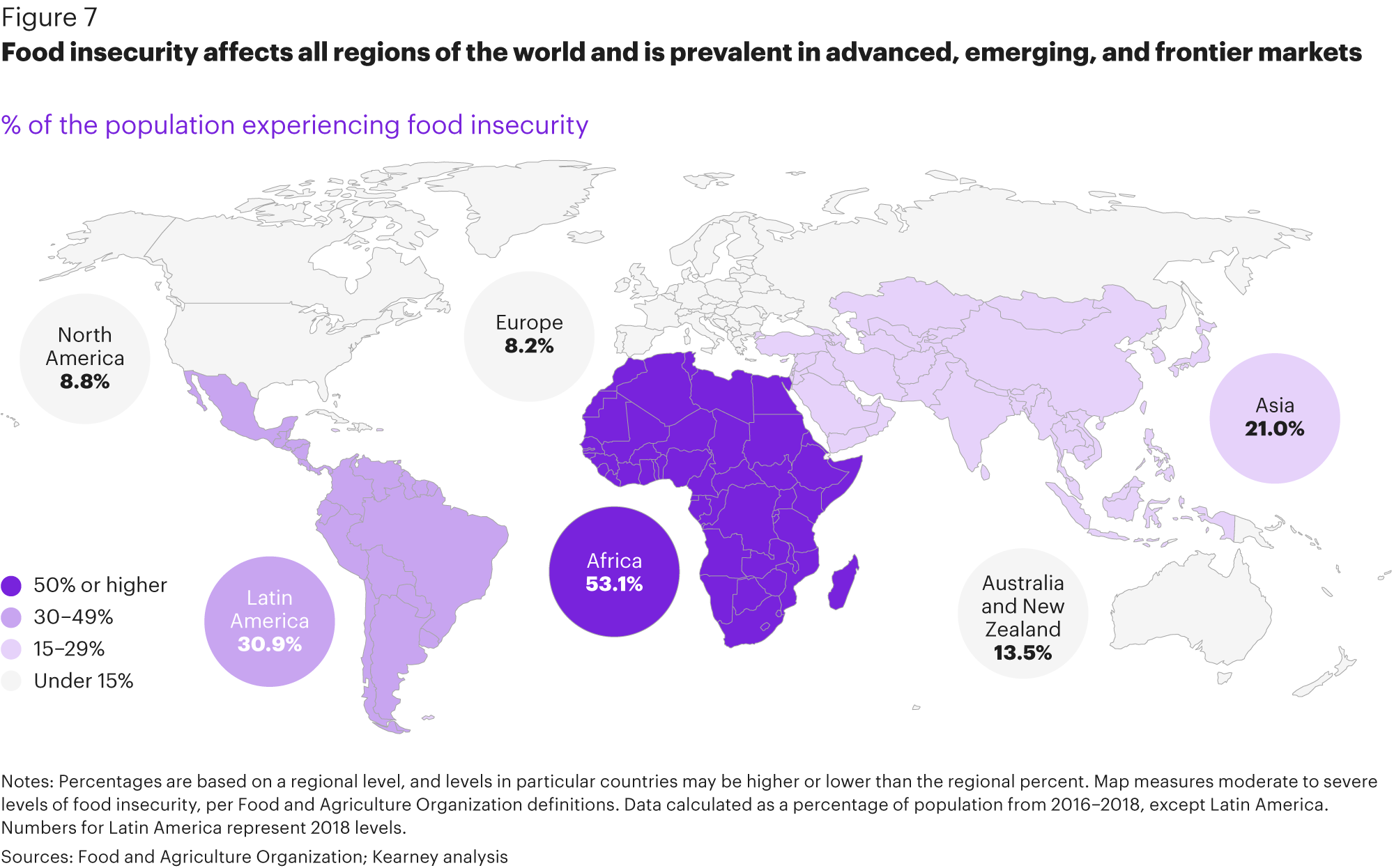

While hunger may not be as prevalent in advanced markets, food insecurity—or the lack of continuous access to nutritious food in sufficient quantities— persists. The Food and Agriculture Organization (FAO) estimates that around 8 percent of people in Europe and Northern America are food insecure (see figure 7). Rates in some countries are even higher: US estimates show that over 11 percent of the population falls into this category, as does 10 percent of Great Britain. One common side effect of food insecurity— especially in advanced economies—is obesity, as families opt for faster, cheaper, less healthy options over costlier healthy foods.

COVID-19 has made these food insecurity challenges in both emerging and advanced economies far worse. Lockdown measures—necessary to slow down the spread of the virus—have prevented agricultural workers from reaching farms. In addition to COVID-19 breakouts at meat plants, micro-level disruptions in planting, growing, and processing food have become more common. For much of 2020, large crop exporters such as Russia limited exports of foodstuff, provoking national stockpiling. These supply disruptions have happened as the global economy is entering a deep recession, leaving many without enough money to buy food. In the United States, between 27.5 percent and 29.5 percent of households with children were food insecure by the end of June, up from around 15 percent two years before. Rising food prices are exacerbating this challenge. In May, US food prices were up around 5 percent year over year, but the United States is hardly alone in this respect. As of October, global food prices are up 8 percent since the height of the lockdowns in May, and experts say this increase is hitting emerging markets particularly hard. Prices of key staples are even higher—the October 2020 FAO Cereal Price Index, for instance, was 16.5 percent higher than October 2019. In Brazil, the prices of staple items such as rice, milk, and tomatoes have risen over 25 percent.

The pandemic will ultimately prove most disruptive to food supply in emerging markets, where hunger was already a concern. Africa is projected to see food insecurity spikes as remittances fall owing to COVID-induced economic disruptions and conflicts in some countries. And those that are in the most dire need of food, such as Yemen and Afghanistan, are struggling to attain it as humanitarian aid gets cut. International aid for Yemen, for example, fell from more than $4 billion in 2019 to just $1.75 billion during the first 10 months of 2020. In the next five years, hunger will plague emerging markets, but embattled governments will find reducing hunger challenging as debt levels surge, currencies weaken, commodity prices remain low, and international institutions find themselves stretched thin.

Food insecurity has commercial implications

In addition to these global consequences, food insecurity has wide-ranging business implications. Hunger has been linked to stunting, a condition that can come with physical and cognitive issues that last into adulthood.4 Globally, more than 20 percent of children under five were stunted in 2019. In some parts of Africa and Asia, the combined productivity and economic losses from stunting can reach as high as 11 percent of GDP. More generally, Chatham House has found that malnutrition in emerging markets can cost companies up to $850 billion in lost productivity. And high food prices, another key driver of food insecurity, have been tied to increased likelihood of civil unrest. Massive protests over food shortages— like those in Chile and Lebanon this spring—can contribute to instability in the operating environment by disrupting business activity and potentially provoking sudden policy changes. In advanced economies, obesity rates can rise as more face food insecurity. Estimates show that the combination of high blood pressure, diabetes, physical inactivity, obesity, and smoking already costs US businesses more than $36.4 billion annually.

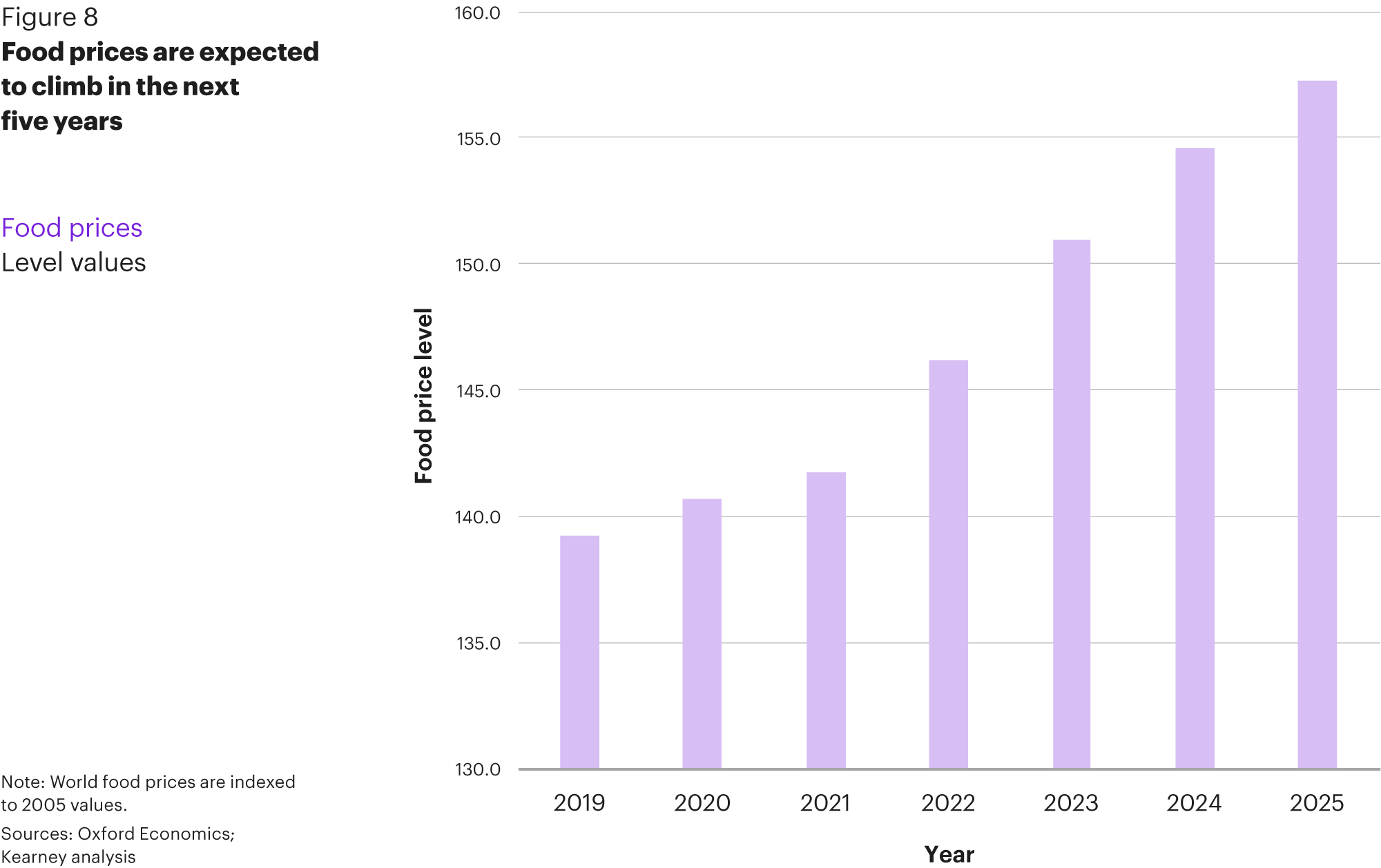

At the sector level, the food industry itself will likely change as a result of this growing insecurity. Consumer preferences could shift toward cheaper items if incomes remain tight and food prices keep increasing, as is expected in the next five years (see figure 8). FAO forecasts that global meat production will drop by 1.7 percent this year due to drought, animal disease, and COVID-induced supply chain disruptions, which could mean higher prices. In the United States, for example, meat prices have proven volatile due to pandemic-related disruptions. The prices of non-meat alternatives, on the other hand, have been steadily trending down since these supply chains have largely escaped pandemic-related challenges. By April, the prices of Beyond Meat burger patty value packs were more or less in line with traditional beef patties, and the company aims to undercut beef prices within five years. The market for plant-based meat substitutes could grow even more rapidly if this trend continues.

The way food is sold and distributed is also likely to change in the next five years. Discount stores and generic brands grow more popular when food prices increase, which could incentivize retailers to reduce prices through promotions or bulk offerings. In addition, pressure to reduce food waste could intensify. Today, roughly 30 percent of food is lost or wasted before it reaches the consumer, suggesting room for improvement. The industry may turn to technologies such as blockchain to track food products. Food supply companies might also try reducing individual packaging sizes to lower costs. And given that consumers are increasingly doing their grocery shopping online, suppliers will have to respond accordingly by going digital. This step comes with steep costs, as items must be refrigerated, products can be fragile, and expiration dates are tight. British firm Marks & Spencer, for example, paid $2 billion for a partnership with Ocado Retail to improve home delivery services. For companies without such deep pockets, micro-fulfillment centers—which pile groceries up in efficient rows— are also an option.

The outlook

Rising food insecurity is already affecting countries globally, and its influence will only increase in the next five years. If the recession proves long lasting, even more individuals could find themselves unable to buy food, especially if handout programs are cut. This trend will create greater inequalities between countries, as emerging markets will have to cope with rising rates of hunger just as their economies are projected to contract. However, advanced economies are still at risk, as food insecurity will still rise in a recession, particularly if governments cut programs such as increased unemployment benefits. Such dynamics not only contribute to social tensions but also exacerbate the health issues that accompany food insecurity such as obesity and stunting. The COVID-induced great shakeout has highlighted the need for stronger food supply chains, as multinational models can be easily disrupted. Therefore, companies will need to learn how to operate locally while better tracing their products to track hiccups along the value chain.

Business implications

- Demand for technology that strengthens food supply chains will rise. As food insecurity grows, companies will face pressure to reduce waste and deliver goods in a reliable and timely manner at a lower cost. Digital technologies, including blockchain products that track items from farm to table, will prove central in these efforts. Italian pasta maker Barilla, for example, has a new digital passport that allows consumers to scan a code and see where the product originated. More firms could introduce similar measures as food becomes an even more precious resource.

- Food processing, packaging, distribution, and sales will evolve as a result of COVID-19. Demand for bulk, non-perishable items and discount products could grow in advanced economies. One study found that soup sales were up 25 percent year over year in July as a result of consumers stockpiling during the pandemic. Firms are also likely to face pressures to change packaging and food sizes to reduce costs by making packaging smaller or offering more family-sized portions, as Mondelez International and Campbell Soup are reportedly considering.

- Companies will face pressure to address health and wellness. As food insecurity worsens, consumers could turn to the private sector to address food-related challenges, as they do today for racial justice and climate change. Companies in advanced markets may follow firms such as LinkedIn, Google, Panda Express, Glassdoor, and a number of smaller start-ups by providing employees with free meals. These programs can boost overall morale and team building. In emerging markets, companies may consider efforts to combat the negative economic impacts of hunger by offering lunch to workers, as some plants in China already do.

Trend #5

Industry consolidations, mergers, and acquisitions

Extended lockdowns amid COVID-19 and other pandemic-related dislocations have squeezed the profit margins of many businesses globally, leading to record levels of corporate defaults. This economic shock is poised to result in a wave of mergers and acquisitions (M&A) as stronger companies acquire weakened rivals, technologies, and assets at bargain prices. Over the next five years, the influence and size of companies and industries already wielding sizable market share are likely to grow as struggling competitors are eliminated during this great shakeout. Depending on the dominance and acquisition appetite of current players, global consumers may face higher prices or fewer market options. Such developments could easily boost government efforts to strengthen national antitrust and foreign investment rules, which have come into the spotlight as the pandemic has exposed vulnerabilities in crucial supply chains—particularly medical supplies—and sparked efforts toward self-sufficiency (see Trend #2).

A COVID-induced M&A wave

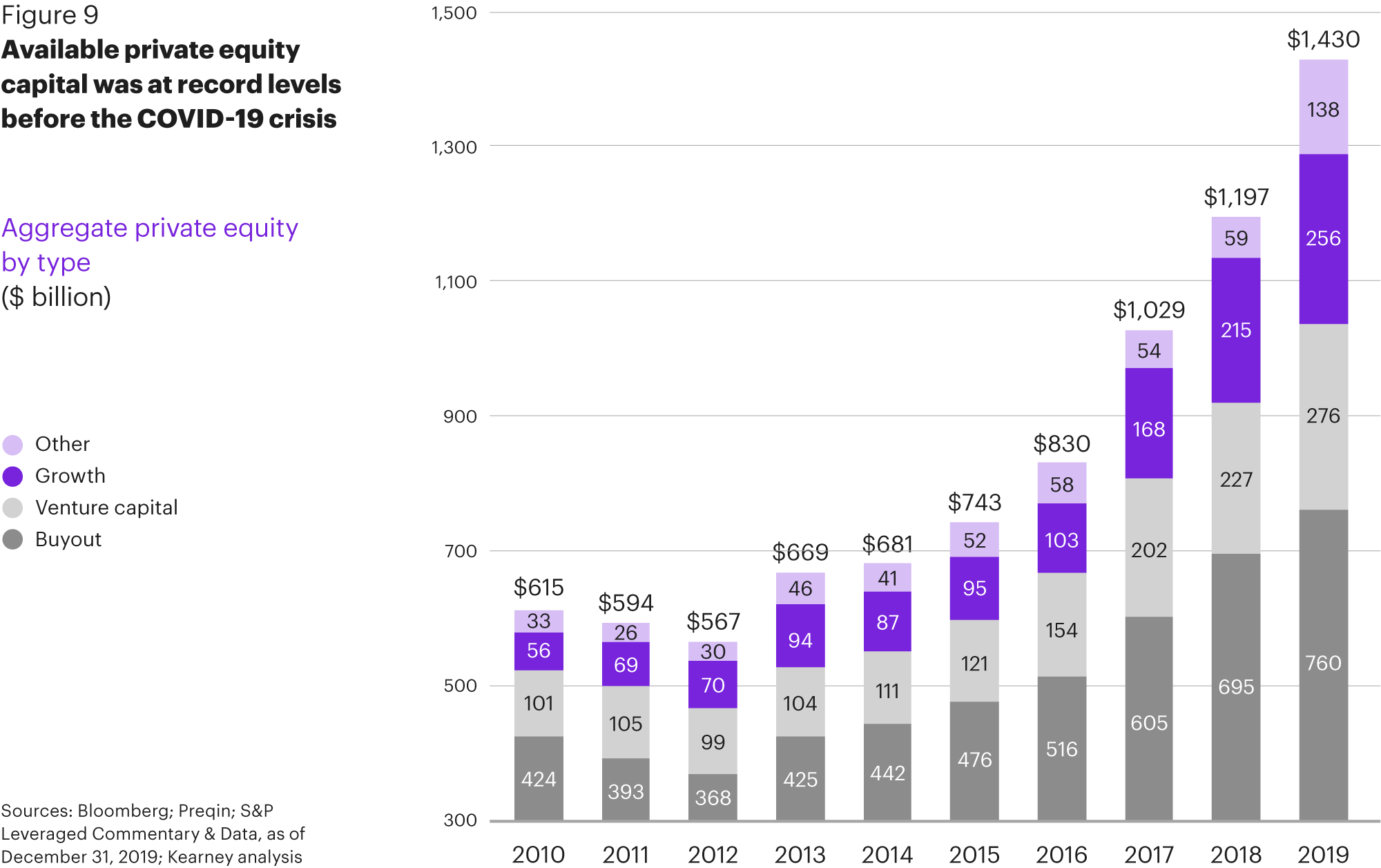

Companies across multiple industries will go shopping for competitors over the next five years. In the meantime, with more than $1.5 trillion in capital and a sea of financially weakened targets made available as a result of COVID-19, private equity groups have deployed their record levels of dry powder in the months following the pandemic, making more than 5,500 deals in the first nine months of 2020 (see figure 9). This activity aligns with a June M&A Leadership Council survey of senior executives, in which almost half indicated that they’d like to “opportunistically buy distressed companies” and close to a quarter were interested in diversifying future revenues. This trend will persist well into the medium term, particularly as uncertainty over a COVID-19 vaccine and its distribution continues. New lockdowns are possible and would further amplify pressures on businesses, small and large.

Stronger companies in sectors benefiting from the pandemic—such as grocers, e-commerce, and digital companies—are also likely to seek growth and additional capabilities by acquiring rivals or new technologies to improve business efficiency. For example, retailer Target acquired the technology of Deliv—a delivery technology start-up struggling in the pandemic. And Chinese conglomerate Fosun said that COVID-19 “spells potentially huge opportunities for every single company” in view of lower business valuations.

Of course, big technology companies are also looking to acquire. Between January and May 2020, tech giants such as Alphabet, Amazon, Apple, Facebook, and Microsoft announced their highest number of acquisitions since 2016—a total of 19. In the third quarter of 2020, both big technology companies and other players continued technology deals, with transactions surging to more than $200 billion—levels not seen in two decades. Such acquisitions are enabling companies to position themselves in areas likely to grow during and after COVID-19, such as automation, fintech, digital services, and food delivery. The activity is further spurred by both the availability of attractive valuations and rising fears of tighter M&A regulations. For example, Facebook spent $5.7 billion on a 9.99 percent stake in India’s digital platform Jio, Microsoft acquired IoT and cybersecurity company CyberX, and European food delivery platform Just Eat Takeaway agreed to acquire the United States’ GrubHub for $7.3 billion. Indeed, tech start-ups that are unable to compete with the giants will become more vulnerable to acquisitions as the latter seek to minimize competition, improve capabilities, and boost revenue streams.

Consolidation will also occur in weaker sectors. Distressed companies will look to merge with other similarly distressed rivals to benefit from economies of scale or seek needed acquirers. For example, travel and tourism plunged by 97 percent in the first four months of 2020, sending airlines, hotels, and rentals into a crisis. By the end of the first half of 2020, tourism was down by 65 percent in 2020 vis-à-vis the same period in 2019. Signs of consolidation have since emerged. For example, in a defensive maneuver, American Airlines and JetBlue announced a partnership to more efficiently manage flights amid the pandemic. Malaysian hotel conglomerate Berjaya Group acquired a majority stake in Icelandair Hotels in April 2020 for $45.3 million after receiving a 10 percent “COVID-19 discount.” And Chinese hospitality chain Huazhu Group planned to open about 1,800 hotels in 2020, capitalizing on independent hotels closing doors amid the pandemic.

Such consolidations will extend beyond travel and hospitality and into other key sectors, including energy. Historical examples, such as Royal Dutch Shell’s acquisition of BG Group in 2016 and Occidental Petroleum’s 2019 acquisition of Anadarko Petroleum, suggest that energy industry consolidation can spike following market and oil price crashes. And after plummeting in March due to a collapse in demand coupled with political tensions, oil prices are expected to remain low. In the first eight months of 2020, 36 US shale oil producers filed for bankruptcy, laying the groundwork for increased M&A activity. Smaller companies that are more affected by oil price swings are likely to go bust or be acquired by larger players seeking efficiency, technologies, or assets. Most recently, US energy giant ConocoPhillips acquired rival Concho Resources, Inc. for $9.7 billion in the largest US oil deal of 2020.

Surf breaks ahead

Obstacles to COVID-induced M&A activity are also starting to materialize, driven by a mix of protectionism and anti-monopoly sentiment. Broadly, industry concentration can lead to inequality, wage reductions, price hikes, and the erosion of consumer power—and policy makers are responding. In the United States in particular, some lawmakers are aiming to prevent such industry concentration. In the US Senate, the Pandemic Anti-Monopoly Act was proposed in May 2020. In October, a congressional investigation into big tech companies recommended breaking up giants and stronger antitrust laws, just before the US Department of Justice filed an antitrust lawsuit against Google. Regulatory scrutiny is intensifying elsewhere as well, with antitrust probes against tech giants, including Facebook, Apple, and Amazon underway in the EU, Australia, Brazil, and Canada. This trend could signal a fundamental change in the makeup of the tech industry, with more smaller players emerging as the bigger firms see their power curtailed.

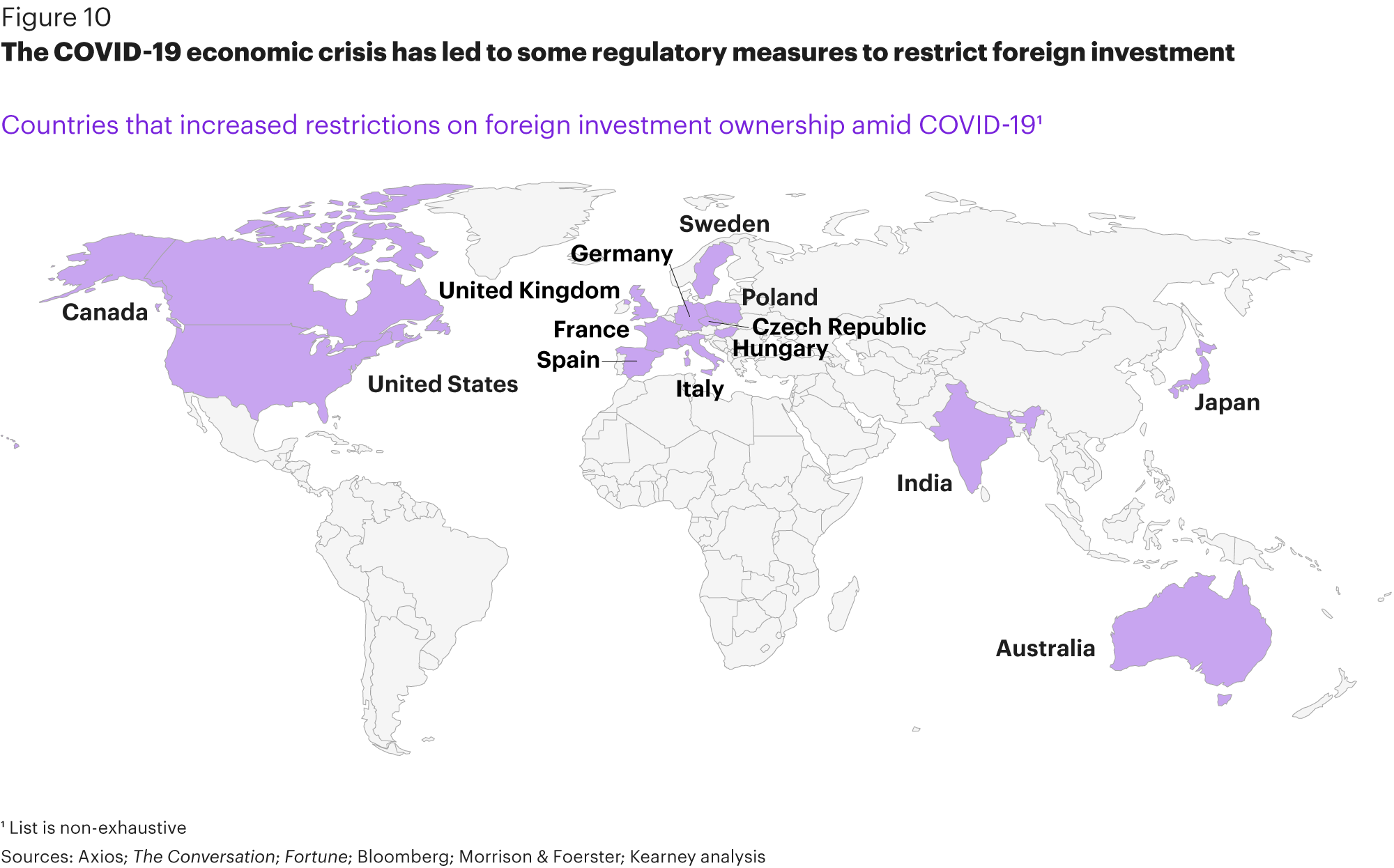

Challenges are also emerging elsewhere. Some governments are pursuing stricter foreign investment rules to protect strategic sectors. The EU as a whole and several European countries have taken such steps amid the pandemic. For example, Germany expanded its rules against non-EU takeovers of companies in healthcare in May 2020, and the country lowered the threshold for a government review process across other sectors. Australia also lowered the deal value threshold for a government review process of foreign takeovers from $1.1 billion to zero in March 2020. In April, India tightened its investment review process for fear of opportunistic transactions, particularly from Chinese companies. The following month, Japan identified more than 500 companies as central to national security and therefore subject to stricter FDI rules. And new rules were introduced in Britain this summer, giving the government powers to examine foreign acquisitions that could jeopardize the country’s ability to manage public health crises (see figure 10).

Some companies are themselves becoming increasingly critical of coronavirus-driven M&A, particularly in the medical sphere. The Pacific Business Group on Health, an industry group whose members include Boeing and Salesforce, has called for a ban on M&A in healthcare, highlighting potential elevated costs of employer-sponsored healthcare for companies already hit by COVID-19. Patients may also suffer greater costs due to healthcare consolidation, as it leads to decreased competition and higher fees. A recent study shows that mergers could raise patient costs between 11 and 54 percent. As healthcare becomes a more salient social justice issue, especially in the United States, M&A—and corporate actions more broadly—that ignore social equity concerns and increasing consumer preferences for social-minded brands may result in negative publicity or consumer boycotts of the acquirer, target, or both.

The outlook

Disruption caused by COVID-19 has left many businesses with shaky finances. Much uncertainty remains regarding the speed and nature of a global economic rebound, with global GDP unlikely to reach pre-pandemic levels until at least 2022 and the effects of the pandemic likely to reverberate far longer. In the meantime, additional lockdowns and further changes in consumer behavior may occur, with implications for spending and investment. Players with more liquidity will take advantage of the situation by deploying longer-range strategies and making acquisitions that improve their existing business models or better position them for the post-pandemic future. Broadly, a wave of M&A will likely result in the realignment of market power in some industries, including healthcare, airlines, grocery, retail, manufacturing, and auto components, which were already among the most oligopolistic industries pre-COVID. And the energy industry—in which previous oil price crashes have fueled M&A—is likely to see one of the greatest shakeouts in the medium term, amplified by continued political and public efforts to decarbonize the global economy and reduce emissions. While emerging regulatory measures—like those in technology—may curb some of the acquisition enthusiasm, the pool of attractive targets across sectors will only grow over the next five years.

Business implications

- M&A success will hinge on understanding post-COVID consumer behavioral changes and shifts in the commercial environment. COVID-19 has transformed industries and consumer behaviors in profound and lasting ways. In order to survive and thrive through future crises, successful acquirers will invest in targets that serve and adapt to evolving consumer preferences for contactless products, improved public hygiene, and better healthcare. Further, government moves toward greater self-sufficiency (see Trend #2) and increased M&A regulation will require deft engagement with governments to pursue targets.

- Optimization and risk preparedness will be new priorities. Companies that have stayed afloat amid COVID-19 and wish to avoid being acquired—or simply seek to remain solvent until the economy returns to growth—will look for ways to optimize costs and reevaluate operations to prepare for future economic shocks. These efforts could include reducing physical office blueprints, consolidating divisions and responsibilities, and renegotiating supplier contracts.

- M&A transactions will carry additional risks. While some companies will find good acquisition targets that will strengthen their positions post-COVID, these opportunities may hide risks, including increased solvency and liquidity risks owing to the pandemic, pre-existing weaknesses in business models, or some combination of both. To mitigate these risks, acquiring companies will need to invest more in due diligence and insurance hedges, and demand greater warranties and representations from target companies. Both will likely require higher legal (and other) fees to secure.

Assessing the status of global trends 2019–2024

The five trends identified in last year’s global trends publication, Resilience, Replacement, and Renewal, remain highly relevant and are continuing to shape the global operating environment. Each of these trends has advanced in the past year, although some more rapidly than others. We present an update on the evolution of each trend below.

- Going cashless. Despite expert warnings that greater economic inclusion must occur before a truly global cashless society can come to be, contactless payments have soared over the past year. As COVID-19 has reduced in-person contact, the volume of e-commerce payments has surged more than 80 percent in Italy and 110 percent in Canada. And in July 2020, Visa reported a 100 percent year-over-year increase in contactless payments for basic items in the United States. Part of this high growth can be attributed to regulatory support, with more than a dozen countries lifting value ceilings and lowering fees on contactless payments amid the pandemic. Even before the onset of the virus, the value of digital payments had reached $4.1 trillion worldwide in 2019, up from $3.6 trillion in 2018. And this value is expected to grow even further to $6.7 trillion by 2023.

- Great battery revolution. Over the past year, many new battery storage projects came online globally. In early 2020, the Asian Development Bank (ADB) approved a US$100 million loan to help Mongolia install its first large-scale advanced battery energy storage system. And NEC Energy Solutions was awarded $4 million to build the largest-ever energy storage system to be financed by crowdfunding in the Netherlands. COVID-19, however, has slowed down some progress in the battery space. For example, monthly electric vehicle (EV) sales—a key use case for lithium batteries—fell by 39 percent in China in Q1 2020. Despite this headwind, industry experts expect that the battery storage market will recover to reach new heights in the years ahead.

- Global re-skilling race. Many companies have announced re-skilling programs over the past year, and COVID-19 has accelerated re-skilling needs as unemployment numbers soar. In January, even before the spread of the pandemic, the US manufacturing industry announced plans to spend $26.2 billion on internal and external training initiatives for new and existing employees in 2020 to combat the shortage of available workers. And in early February, French telecoms firm Orange publicized a €1.5 billion re-skilling plan to strengthen its employees’ technology expertise. Amid COVID-19 and growing protests over structural racism, companies such as Indian IT consultancy Infosys have set new upskilling targets to reach key groups such as women, non-degree holders, and minorities. The virus and the displacing effect it has had on many workers in industries such as retail, hospitality, and tourism will undoubtedly lead many governments and businesses to reevaluate their skills needs and determine how current and future employees can be best utilized in new essential industries such as healthcare and medical research.

- Rise of climate-resilient infrastructure. Though the pandemic has fueled fears that efforts to prevent and mitigate climate change will fall by the wayside, development of climate-resilient infrastructure has not taken a significant hit— especially among smaller nations. On June 3, 2020, US Congress’s House Committee on Transportation and Infrastructure introduced the INVEST in America Act, a five-year, $494 billion surface transportation bill that aims to transform America’s aging infrastructure by funding projects that increase the safety, reliability, and resilience of surface transportation while mitigating climate change. Smaller nations are also taking action. In the face of persistent extreme weather events, Dominica has recommitted to its goal of becoming the first climate-resilient nation by 2030. And in July, UN-Habitat launched a four-year, $14 million project to boost urban resilience, reduce disaster risk, and increase climate change adaptation in Madagascar, Malawi, Mozambique, and the Union of the Comoros.

- Loneliness epidemic. The loneliness epidemic has combined with the COVID-19 pandemic to create a real danger to mental health over the past year. Social distancing requirements and full-blown lockdowns have led to Germany seeing calls to its mental health helpline rise by almost 20 percent. And one in two Australians report feeling more lonely since the onset of the virus, with young adults aged 18–25 feeling this isolation most acutely. The elderly are also experiencing heightened loneliness, as their physical vulnerability forces them to isolate and remain disconnected from family. Start-ups such as Norwegian No Isolation have stepped up to combat this increased pandemic-induced loneliness by boosting production of items such as telepresence robots for children and simplified tablets for the elderly.

About global trends

Global trends 2020–2025 identifies five macro trends that play an outsized role in the current and future operating environment for businesses, governments, and citizens around the world.

As part of its core mandate to help leaders anticipate and plan for the future, the Kearney Global Business Policy Council continually scans the horizon for developments across the global external strategic operating environment in the key dimensions of demography, economy, environment, geopolitics, governance, resources, and technology. In assessing these dimensions, the Council identifies emerging trends on an annual basis that may be slightly below the radar but are likely to have significant implications for how businesses and governments operate in the next five years. Global trends 2020–2025 explores the manifestation of each of this year’s trends today, analyzes its medium-term outlook, and presents its high-level implications for business and government. This publication also revisits the trends that the Council identified in last year’s report to assess their trajectories over the past year and update their prospects.

The goal of the Council’s annual global trends publication is to help business and government leaders and strategic planners question their assumptions and build their capacity for adapting to the future—whatever it may bring. As such, the Council’s global trends analysis can help organizations develop monitoring systems for the evolution of trends—and the strategic shocks they may generate—that are most germane to their sector or industry, mitigating downside risks, recognizing opportunities, and strengthening their long-term strategies.

The authors wish to thank Terence Toland, Gabriella Huddart, Rebecca Grenham, and Radina Belberova for their valuable contributions to this report.

1 The Group of Seven (G7) is an international intergovernmental economic organization comprised of Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.

2 OPEC+ describes a loose organization of OPEC producers and other oil producers, including Russia.

3 Per the Food and Agriculture Organization, undernourishment is how the group measures hunger. Undernourishment measures the proportion of the population that consumes less in dietary energy than a set, preconceived level. Hunger is defined as food deprivation scientifically, or an uncomfortable (and often painful) sensation resulting from inadequate food energy consumption.

4 According to the World Health Organization, children are considered stunted if their height-for-age is at least two standard deviations below the global median.